| |

Production

Sharing Basic Term |

|

There

are some principles underlying the Production Sharing

Contract:

|

| |

- Production

Sharing Contract was setup within the concept of

the Indonesian Law No.44/Prp/1960, Law No. 8/1971,

Law No.7/1983 and Ministerial thereto.

- Pertamina

on behalf of the Government of Indonesia shall be

responsible for management of the operations in

the Contract Area.

- CONTRACTOR

shall be responsible for the execution of the operations,

and shall provide all foreign exchange, technical

assistance and carry the risk of all exploration

costs.

- Indonesian

participation: 10%.

|

| |

The

Government of Indonesia/PERTAMINA in securing its objectives

as well as the Contractor's under said dynamics, has from

time to time modified the PSC, not in terms of its principle

features, but more in its fiscal terms. Such modifications

were made to adopt to prevailing situational issues, such

as fluctuation in crude oil price, taxation, etc., as

well as to non-situational factors such as the natural

conditions of the acreage implying the risk and cost of

exploration.

|

|

|

|

|

|

Arrangements

|

|

There

are five arrangements of the contract as follows:

|

|

1.

Contract of Work (COW)

|

|

-

Companies are Contractors to Pertamina

-

Contractors are responsible for management and operation

- 60%

of balance is paid to the Government

- 25%

of the 40% is taken for Domestic Market Obligation

(DMO)

@ US$ 0.20/bbl reimbursement

- Minimum

Government income is 20% of the total revenue

-

This type of contract is no longer applied.

|

|

|

|

2.

Production Sharing Contract (PSC)

|

| |

-

Corporative agreement in the sector of oil and natural

gas between Pertamina and foreign capital investor,

in which:

-

Pertamina is the management

-

Related foreign oil company is contractor responsible

to Pertamina

-

Sharing is made on production, not on profit

-

Title to contractors portion of crude oil and gas

(cost and entitlement oil/gas) shall pass to contractor

at the point of export or point of delivery

-

Laws, decrees, regulations and decisions of Republik

of Indonesia shall be applicable

|

|

|

|

3.

Technical Assistance Contract (TAC)

|

| |

-

Sharable crude is crude other than primary crude

- Cost

of equipment and services for the primary crude will

become part of the operating cost

-

Maximum operating cost is 60% of total sharable lifting

cost

- On

obligatory DMO contribution @ 15% export price is

taken from the contractor's share. After cost recovery:

- Pertamina

: 85%

- Contractor

: 15%

|

|

|

|

4.

Joint Operation Assistance (JOA)

|

| |

-

Pertamina holds 50% participating interest

- The

participating interest of contractor is subject to

the same terms and split as used in the PSCs

-

Pertamina is the operator assisted by the contractor

in the form of a Joint Operating Body (JOB)

- JOB

is responsible to, and supervised by Joint Operating

Committee (JOC)

-

Pertamina and contractor are the member of JOC

- JOC

approves Work and Program Budget, and holds policies

- Contractor

carries Pertamina in financing exploration, ventures

and advance development projects

-

Pertamina's sunk cost is recoverable and 50% uplift

is applicable

|

|

|

|

5.

Enhance Oil Recovery (EOR)

|

| |

-

The scope of project is: pilot phase, injection water,

fluid handling and treating facilities, drilling,

work-over of injections and production wells

- Injection

system, flow lines until the connecting flanges to

the manifold inlet of Pertamina gathering station

-

Incremental oil production: is determined for each

production zone and agreed prior to contract signing

-

EOR cost and incremental oil produced are governed

by the same terms as the JOA, except that 65% cost

recovery ceiling is applied in the EOR

-

Cost incurred by Pertamina downstream is chargeable

to EOR operation on pro-rata basis

-

The initial to yield contract is allowed to the pilot

phase, thereafter full EOR project will commence

|

|

The

Indonesia government applied the New Taxation Law and

Regulations for the PSC with a tariff of 48% in 1984.

However, the new regulations were applied only to PSC's

signed after 1988 because during the process of negotiation

the contractor tended to apply the old taxation regulations.

Since the government carried out the rule of Income Tax

Law No. 10/1994, the new taxation for the PSC is 44%.

|

|

Thus,

the standard sharing of production changed into the following:

|

|

-

Oil : 65.9091% for Government, and 34.0909% for the

Contractor

-

Gas: 20.4545% for Government, and 79.5455% for the

Contractor

|

|

The

net share after deduction of tax:

|

|

-

Oil: Government/Contractor = 85/15

-

Gas: Government/Contractor = 65/35

|

|

|

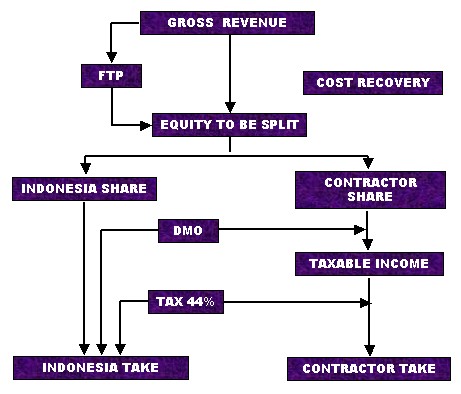

| |

Flow

of Revenue of PSC |

|

|

| |

|

|

|

|

|

| |

Exploration

Incentive Packages |

|

Knowing

that exploration for oil and gas is a risky venture, the

government of Indonesia has offered four incentives to

oil companies since 1988.

|

| |

-

The first incentive package introduced in August 1988,

included deregulation measures to be taken in the

procedure.

-

The second incentive package issued in February 1989,

addressed the equity split for mafriban fields, oil

produced from Pre-Tertiary reservoir rocks, Tertiary

EOR projects and investment credit incentives for

deep sea contract areas.

-

The third incentive package introduced in August 1992,

was intended to stimulate activities in gas exploration

in both conventional and frontier areas with better

equity split and the improvements of investment credit

and DMO

-

The fourth incentive package appeared in late 1993.

This package is based on geological thinking with

geographical considerations. The archipelago is divided

into the Western part as defined by the Sunda Platform

and the Eastern part, that is the area east of 200

m isobath and other frontier areas in Western Indonesia.

The DMO fee in the fourth package was increased from

15% to 25% of export price, while the First Tranche

Petroleum (FTP) was decreased from 20%

|

|

The

following table is the incentive packages:

|

|

|

| |

|

Element

|

1st

Incentive Package

(August 1988)

|

2nd

Incentive Package

(February1989)

|

3rd

Incentive Package

(August 1993)

|

4th

Incentive Package (December 1993)

|

Investment

Credit

|

Investment

Credit amounting 17% of the Capital investment cost

|

For

deep sea areas over 600 ft:

|

Development areas :

- Pre-Tertiary

reservoir rocks = 110% for oil and gas

- Water

depth 200-1500 m = 110% for oil and gas

-

Water depth below 1500 m = 125% for oil and

gas

|

No

longer applied

|

Commerciality

|

Condition

that the government has to obtain as minimum of

49% of the gross revenue not valid anymore. The

minimum guarantee is 25% of the gross revenue for

the government

|

Abolished

|

Abolished

|

Abolished |

Domestic

Market Obligation (DMO) Prices

|

10%

of export price after this first five years

|

10%

of export price after this first five years

|

15%

export price after the first five year.

|

25%

export price after the first five year.

|

First

Trache Petroleum (FTP)

|

20%

of production taken before deduction of cost recovery

and will be split between government and contractor

|

No

change

|

No

change

|

15%

of production taken before deduction of cost recovery

and will be split between government and contractor

|

Split

for Oil

|

Frontiers

Production:

|

Marginal

Fields and EOR in Tertiary Reservoir:

Conventional

Area = 85%:15%

Frontier

Area = 75%:25%

Pre-Tertiary

and deep sea (over 600 ft) production: Incremental

split as same as frontier production in the first

package

|

|

65%:35%

without Investment Credit

|

Split

for Gas

|

Frontiers

Production = 70%:30%

Conventional

Areas = 70%:30%

|

No

change

|

Frontiers Production:

-

Field developed in conventional areas = 65%:35%

- Field

developed in frontier areas = 60%:40%

-

Field developed in areas with water depth >

1500 ft = 55%:45%

|

60%:40%

without Investment Credit.

This

split is applied for Eastern Indonesian areas

and path of Western Indonesian areas having similar

geological and geophysical conditions.

|

|

|

|

|

|

|

|